Terror in the Supermarkets: What Is Happening in the AI Bubble and Why Should You Care?

We have a drama unfolding: at the very moment companies are preparing to go public, the AI bubble is starting to look like a zombie.

The original (Spanish) version of this article can be found here.

You are probably not one of those people who follows what happens in the stock markets. No judgment :p. But I think this week it’s worth paying attention. We are approaching the end of a cycle that is going to change everyone’s lives — for better or for worse — and its consequences are going to make themselves felt in the months ahead.

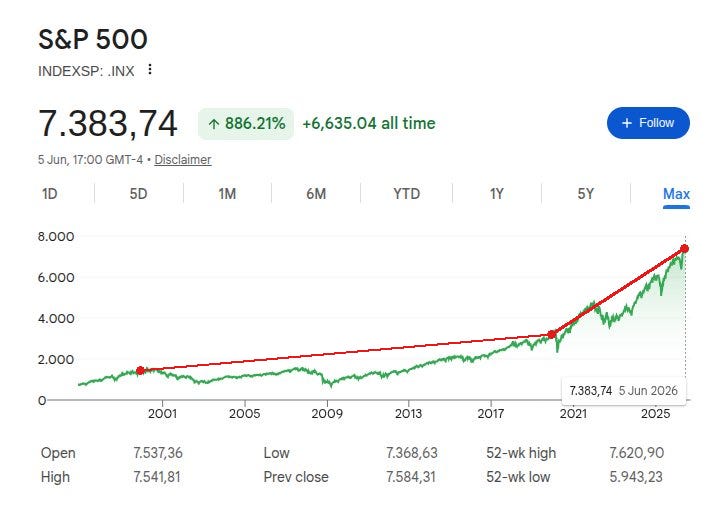

Take a look at this image:

This is the S&P 500 — the index that brings together the 500 most important companies in the United States. As you can see, until 2020 it had been growing at a more or less steady pace: in twenty years it hadn’t even managed to double its value. But since March 2020, something has happened that has been pushing it upward — its value has tripled in five years.

This phenomenon, visible across all Western stock markets, has a fairly obvious cause: the great economic narrative of our time holds that an anticipated “AI revolution,” driven by a handful of listed companies, will come along and transform everything. The rise of inequality, the concentration of power in a handful of tech billionaires, and even the fuel feeding Trumpism are all the fine print of that same story.

The consequence: after this revaluation, those markets are today worth, collectively, nearly $100 trillion — as much as all the housing stock in the United States and Europe combined, and 15% of all the wealth in the world.

A tremor shook that pile of money this week. On Friday, Wall Street had its worst day since October: the S&P 500 fell 2.6% and closed at those same 7,383.74 points you see in the image. But the hardest blow fell on technology. The Nasdaq — home to the big tech companies — plunged 4.2% in its largest single-day drop in a year. At the epicenter of the earthquake, the companies that manufacture AI hardware — the beating heart of the artificial intelligence bubble — shed as much as 10% in a single session.

This is the first of a series of events that, in the coming weeks, will precipitate the resolution of this bubble and this narrative — in one direction or another, for better or for worse. That is why, and because there will clearly be a great deal of news on these subjects, it is worth understanding what is happening in the markets.

Buckle up! here we go!

All the Horsemen of the Apocalypse

Like the program notes for an opera, let’s start by describing the characters. There are five types:

The LLMers: OpenAI (ChatGPT) and Anthropic (Claude) are the creators of the chatbots and AI models that have astonished the world.

The manufacturers: Nvidia, Broadcom, and AMD manufacture and sell the hardware installed in data centers to train and run those models.

The data centers: Oracle and CoreWeave build and rent out data centers — enormous facilities packed with hardware where it is all installed.

The giants: Google, Microsoft, Meta, Amazon, and SpaceX (owner of X) have the capacity to put this technology in the hands of customers — and charge for it. (Though these last are so large they are playing all four roles simultaneously: building their own chips, constructing their own data centers, and training their own models.)

The financiers: behind all of the above, in the shadows, are other characters putting up the money — the investors and the lenders.

So far, here are the characters who star in this story:

Act One: The Bubble’s Moment of Truth

This Friday, SpaceX — the space conglomerate that Elon Musk has been frantically trying to rebrand as an AI company — goes public. Three years after the launch of ChatGPT, the first major company in the sector floats at the highest valuation in history, comparable to the GDP of a Eurozone country: $1.8 trillion.

As one analyst on X explains after studying the documentation Musk filed with the regulator to justify that valuation, this operation is not quite what you’d expect:

“After eighteen images of rockets in space, we discover that the company’s mission is to ‘extend the light of consciousness to the stars.’ To achieve this, the company plans to advance humanity ‘to Type II status on the Kardashev scale,’ which the document defines as ‘a civilization that harnesses all the energy emitted by its local star.’ We’re only a few pages in and it’s already starting to feel like an ayahuasca trip.”

This is, self-evidently, not a business proposal. It is an incomprehensible chimera. A messianic cult. A — bad — science fiction novel. An absurdity.

A necessary one, however, because companies typically go public at a valuation equivalent to roughly six times their revenue — but SpaceX is claiming to be worth 97 times what it billed last year. It is madness; which is precisely why it requires all the imagination in the world to be even remotely plausible.

Beneath the surface, many observers — from the analysts at More Perfect Union to those at the Financial Times — are saying that this is the first operation designed to allow the financiers who have put their money into AI over these years to cash out by offloading their shares, wrapped in this interstellar fairy tale, onto the small retail investors who have their savings in the stock market.

Anthropic Is Also Preparing Its IPO

SpaceX is only the first major operation in the sector. Anthropic — the frontrunner among the LLMers — has also filed its own paperwork this week to do the same, at another astronomical valuation: over $1 trillion. It won’t be in June — there isn’t time — but it is expected that, if nothing goes wrong, it will list in the first weeks after the summer. It looks as though it will get there ahead of OpenAI too, which announced twenty days ago that it would file its documentation but still hasn’t.

On top of that, some of the giants — including Google and Meta — have announced that in the coming months they will issue new shares to finance their data center investments. The moment of truth for AI companies has arrived, and everyone is a little on edge.

Show me the Money

Here is the drama of our little operetta: at the very moment the main characters are preparing to hit their high note on the stock market, the AI bubble is starting to look like a zombie.

If last week the Financial Times described the LLMers’ numbers as “impossible,” this week the world’s third-largest consulting firm has once again confirmed something that is becoming increasingly obvious: companies are still not finding a return on this technology.

That sentiment was embodied a few days ago by the CEO of Uber, who admitted that no matter how many tokens his engineers consume, “that link — the one connecting that spending to products that are actually useful for customers — isn’t there yet.” He then did what many other companies are now doing: turned off the tap by capping token spending per employee per month. This is the end of “tokenmaxxing” — the practice that encouraged spending as much as possible. Token demand is expected to moderate in the coming months.

Perhaps as a consequence, two major investors have sounded the alarm in the past few hours. Ray Dalio, founder of the world’s largest hedge fund, has conceded the obvious — that there is a bubble that will eventually burst — while the Chief Investment Officer of Bank of America, famous for having coined the term “Magnificent Seven,” sent a note to clients a few days ago recommending they position themselves for a market crash.

After the euphoria of a couple of months ago around Claude Code, the shift in how AI is being perceived is very clear. As Tom Cruise demanded in Jerry Maguire: it’s time to show us where the money is in all of this.

Act Two: The Tremors

On Wednesday, something apparently innocuous happened. Broadcom — one of the manufacturers — reported another extraordinary set of results: billions in revenue and record growth. But there was a tiny catch buried in the accounts: the company did not raise its forecast for the rest of the year. It didn’t lower it — it remained enormous — it simply didn’t raise it. There was no “beat and raise,” in the market’s jargon, that ritual investors have grown dangerously accustomed to, in which each quarter AI companies not only beat expectations but promise even more for the next one.

But the market is as sensitive as I am in the week before my period. Faced with the first piece of news that didn’t quite land the way it wanted, it did exactly what I would have done in my situation: it burst into tears. Broadcom lost 20% of its market value in two days, dragging other manufacturers down with it.

Bad News: It Looks Like AI Isn’t Going to Take Your Job After All

The other bad news of the week wasn’t really bad news either. On Friday, the US employment figures for May were published. And the bad news — for the markets — was that they were far too good: 172,000 jobs had been created, against the 80,000 that had been expected.

That means two things. First, that the labor market is still standing: AI is not emptying offices of workers. But then it isn’t cutting costs, nor supercharging productivity, the way its evangelists promised. Second — and more immediately — with inflation still proving sticky, the Iran war ongoing, and employment this strong, the possibility of the Fed raising interest rates in the coming weeks is growing more solid.

Terror in the Supermarkets.

These two apparently innocuous pieces of news — which in any other moment would have passed unnoticed — combined on Friday with the nerves unleashed by the SpaceX IPO and the growing sense that the AI bubble is ending to wipe out nearly a trillion dollars from the markets in a matter of hours. And the most striking thing was that nobody even seemed surprised, because the trend of recent months had been one of complete schizophrenia.

Bitcoin, which in October was approaching $126,000, is today trading at less than half that. Gold — which had been setting record after record — did the unthinkable for a safe-haven asset and started falling precisely at the moment of greatest fear. US debt yields have been at century highs for weeks, and on the other side of the world, the South Korean stock market has become the most extreme spectacle of all: after surging 109% in barely six months, it suffered a crash this week severe enough to trigger an automatic trading halt. The feeling is that nobody is at the wheel, or that every investor is pulling in a different direction — as if money, frightened, no longer knows where to hide.

Comparisons with the peak before the dot-com crash have been the theme of the week, and beneath the apparent acceleration of the markets lies fear: terror in the supermarkets.

Rotation or Stampede?

There are two ways to rationalize all of this. The first — if you believe the LLMers’ valuations make sense — is that investors are divesting from less profitable things to get into SpaceX this Friday, and that the IPO will be a success. This is what the jargon calls “asset rotation.”

The other is that the major financial players are growing increasingly convinced that the bubble will burst very soon, and are abandoning the positions they see as most at risk — starting with the hardware manufacturers.

The End of Trump

On the horizon: the “midterms”. The elections that every two years renew half of the American Congress and Senate. They are in November, and they are shaping up as a financial cliff edge — because the markets’ bull run in recent months has been driven in large part by Donald Trump turning every week into a succession of promises and headlines designed to keep the rally going.

This very weekend — spooked, no doubt, by what happened on Friday — he has made one of those announcements we’ve grown accustomed to: the United States is considering investing in the LLMers, and perhaps in the manufacturers too.

This statement is almost like a preemptive bailout announcement — a guarantee to potential investors that they won’t lose their money if they bet on AI. But today, trapped in the Iran war and with his approval ratings at rock bottom, the chief cheerleader of the financial markets has a high probability of losing control of Congress and the Senate in November. How many TACOs are still left in the kitchen?

What Is Actually Happening?

Behind that specific trigger, however, something deeper is pulsing — something we’ve discussed here before. The AI bubble was inflated on the promise of “singularity,” “superintelligence,” and “the replacement of humans.”

None of these things have happened, and there are no signs that they will. It’s time to recalibrate expectations, and the conclusion — now increasingly widespread — is that the companies that drove this entire rally are overvalued. In this environment, things have been happening for weeks for which nobody really has a satisfying explanation.

Right now, two forces are colliding — an unstoppable object meeting an immovable one: the peak of expectations, represented by the IPOs of the sector’s key companies, meeting the hardening of underlying reality — the hard data on AI’s actual use and effectiveness.

What Will Happen in the Coming Months?

I am not a market analyst. If I have said many times — since 2024 — that I believe all of this is a bubble that will burst, it is not for reasons of financial timing but because the deep currents that have moved the economy and society over the past twenty-five years can only keep producing one bubble after another. AI is just the latest explosion.

But following these things closely leaves a mark, and my intuition tells me that the SpaceX IPO will succeed. Largely because Trump has committed himself to saving it, but also because there are many people who want to believe this is their chance to invest in something like what Google was in 2005. And Musk knows how to play that game better than anyone. I also believe those same people will lose their money, because SpaceX is not worth $1.8 trillion and the market will eventually correct the price sooner rather than later.

But for the bubble to truly burst, there is still a missing piece in this whole soap opera: a “black swan” — an unexpected, uncontrollable event similar to what the surprise bankruptcy of one of America’s largest banks, Lehman Brothers, represented in 2008.

An Unanswered Question

And that black swan is not, I think, among the things being talked about — but in one that isn’t.

OpenAI was the frontrunner among the LLMers until very recently. But in just a few months, Anthropic has overtaken it and today dominates the market. Since then, life inside OpenAI must have been something of a hell — like a runner watching someone overtake them and falling ever further behind.

OpenAI is losing users, has had to shut down some of its flagship services, and is not hitting the revenue targets it had set for itself. As if all that weren’t enough, The New Yorker published an extraordinary piece a few weeks ago claiming that its CEO, Sam Altman, is a sociopath and a pathological liar — and it leaked to the press that its CFO, Sarah Friar, had clashed with him and the two were no longer even in the same meetings.

The reason for the falling-out was that Friar believed it was more sensible to delay the IPO to 2027, while Altman wanted to go as soon as possible.

Everyone knows that in a startup on the verge of going public, it’s the CFO who calls the shots. So a few days later, someone (wink, wink) leaked to the Wall Street Journal that OpenAI was going to file its IPO papers immediately.

Nearly twenty days have passed, Anthropic has taken the lead, and OpenAI? Nothing. Not a word since.

My suspicion — with zero inside information, but considerable experience managing companies through difficult moments — is that OpenAI is in very deep crisis. It is highly likely that investors are completely frantic at the prospect of Anthropic cannibalizing them, which is exactly what’s happening. It wouldn’t surprise me at all if they are simultaneously struggling to raise financing and running low on cash. With a CEO who was already thrown out by his own team for being a sociopath a few years ago, I would bet that this whole situation resolves itself in one of several ways: either Friar walks, or Altman is ousted again, or a revolt among engineers hollows out the team.

I think OpenAI will be the new Lehman Brothers.

And I’ll be here to tell you about it when it happens. Don’t forget to subscribe!

If you want to understand why I think we’ve been living inside a bubble for twenty-five years — one that will keep bursting until we deflate it — you can’t miss Hijos del optimismo (Children of optimism).