Properly. Masterclass to understand the housing problem.

All the questions and answers you need to be able to speak authoritatively about the housing crisis: its causes, its consequences, and the reasons why it is spreading throughout the world.

The original (Spanish) version of this article can be found here.

A nation of homeowners, of people who own a real share in their land, is unconquerable.”

Franklin D. Roosevelt

Housing has become the defining problem of global society — and apparently overnight. Perhaps that is why there is so much confusion, and why it is so difficult to understand, let alone explain, what is actually happening. How did it become a crisis? Why does it affect every country? Why do prices keep rising without end? Can building more fix it? What about liberalizing the market?

When a problem is hard to understand, it is often because we are thinking about it in the wrong way. And I believe that is precisely what has been happening here for a long time. The other day, Bosco Gámiz suggested I write a piece answering some questions, which other readers then expanded upon with ideas of their own.

And I — who always wanted to write a book called The Housing Theory of Everything (and would have done so had I found a title equally catchy in Spanish) — got carried away, and what began as a Q&A ended up as a masterclass. A manual. Everything you need to know to understand, as well as any specialist, a problem that has become universal and now threatens our world.

Here it is! I hope you like it.

Why Is the Housing Problem So Hard to Understand?

Because we are approaching it in the wrong way.

Some argue that housing is a market good, like cars or oranges. It is not. Others compare it to an “asset,” as though it were a printing press or a gold bar. That does not hold either. For housing to be comparable to those goods, it would need to satisfy one basic condition: that supply could rise or fall freely in response to market forces. But it cannot. Housing does not follow market logic, because its supply is constrained by the number of available licenses.

In fact, although — as so often happens — its physical materiality clouds our judgment, a dwelling is first and foremost a title: an authorization, a permit, a license. Without a license, a building cannot legally function as a home in any developed country. The housing market is therefore, in essence, the market for residential licenses.

And those licenses constitute a monopoly. It is states that issue them. This is why housing resembles neither consumer goods nor investment goods, but rather the share capital of companies. The best analogy for understanding housing is to think of it as stock in a company — and that company is a country.

Just as companies divide their ownership into shares priced according to the firm’s value, countries issue housing licenses whose value is tied to the city and country in question. Just as companies stand behind the price of their shares and regulate it, so too do countries. Housing is a country’s stock — and the real estate market is something very close to a stock exchange.

It is not a bug, it’s a feature.

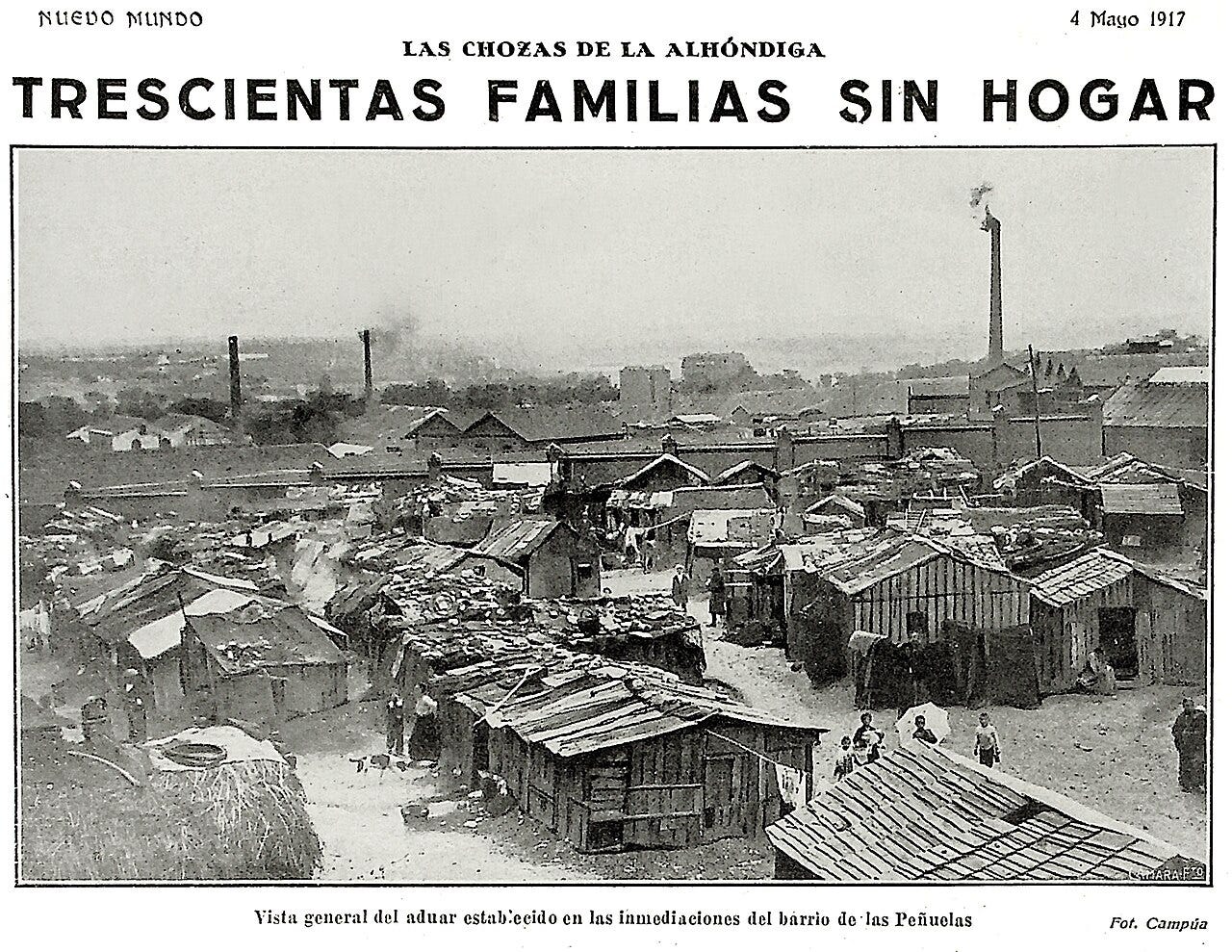

The story goes like this. The first half of the twentieth century was a period of sweeping change across the Western world. Much of the rural population moved to the cities, industrial labour began to replace agricultural work, and the modern metropolis was born. In the midst of that transformation, the crash of 1929 unleashed a tsunami of poverty and dislocation on both sides of the Atlantic that ultimately pushed the world toward the Second World War. When the conflict ended, with part of the territory destroyed by bombing and the rest still waiting to be built, an entire world remained to be made.

And it was made — literally. In the years that followed the war (known as the “Trente Glorieuses,” or the Glorious Thirty), health systems, education systems, universities, transport infrastructure, sanitation networks, energy grids, legal institutions, and industries were all built from the ground up. Everything. The countries we inhabit today were founded in that period.

Spurred by the fear of another war and by the pressure exerted by the Soviet bloc, political elites designed a plan to bring the working classes into a share of the gains from progress. They struck a pact with their citizens — one that held for half a century — under which the ownership, both literal and figurative, of their countries would be distributed through housing.

For those in power, distributing homeownership was the means of securing popular commitment to a political model. For citizens, it meant acquiring a share that conferred a stake in the country’s future.

This is why Franco declared that Spain would move from being “a country of proletarians to one of property owners”; why Margaret Thatcher wanted “every man and every woman to be a capitalist,” and saw housing as “the starting point” for achieving that; and why, for both left and right alike, housing was, in Roosevelt’s words, “a participation in the future.”

And so the world embarked on a colossal “share issuance.” In Europe, for example, between 1950 and 1990, seventy percent of the current housing stock was built — far exceeding what had existed before. In 1945 there were fewer than thirteen million dwellings; by 1990 there were five times as many. For several decades, construction outpaced population growth.

In a handful of northern European countries, that housing stock remained in state hands, forming a public park of social housing. But in the vast majority of countries, it was distributed at cost price among the young adults of the time — like a gigantic universal inheritance. That is how two generations came to own the entirety of the Western world.

Today, housing is still this. It is a title of ownership over a small piece of a state — with its investments, its human capital, its national brand, its commercial and political agreements, and everything else that entails. This is why people who own a home feel like owners in a sense that extends far beyond their four walls. This is why housing rises or falls in line with how a country is faring. It is exactly what happens with a company’s shares.

Why Has Housing Become a Problem?

Until the end of the century, housing was not a particularly valuable stake. People had never paid much for their homes because cities were small and space was plentiful. In almost every city there were still peripheral districts and undeveloped areas that had gradually been occupied by waves of migration. The norm, in the 1950s and 1960s, was to pay very little for a rental.

In 1970, for example, the United States’ 22 million renters paid an average of around one hundred dollars a month, including utilities — roughly eight hundred dollars in today’s money, or about 12 percent of a median American family’s income.

The real sources of money in the twentieth century were natural resources, concessions on major infrastructure projects, factories, and construction companies — the firms of the industrial economy. Housing was the equivalent of what, in a company, would be “subordinated” or “Class B” shares. In other words, there was a first-tier capital — more expensive and more profitable — that consisted of companies, where large fortunes were invested; and then a Class B issuance was created for ordinary people to invest in: that was housing. The pact, in essence, was that the upper classes would retain the majority of each country’s capital, while the working classes would receive a subordinate and modest share.

But at the turn of the millennium, a perfect storm gathered, driven by several converging phenomena.

The industrial economy began to retreat. Factories disappeared from the Western world, and natural resources grew cheaper. At the same time, a new economy was emerging — one that no longer required the vast investment that factories once demanded. The true oil of the twenty-first century was no longer extracted from a well: it was knowledge.

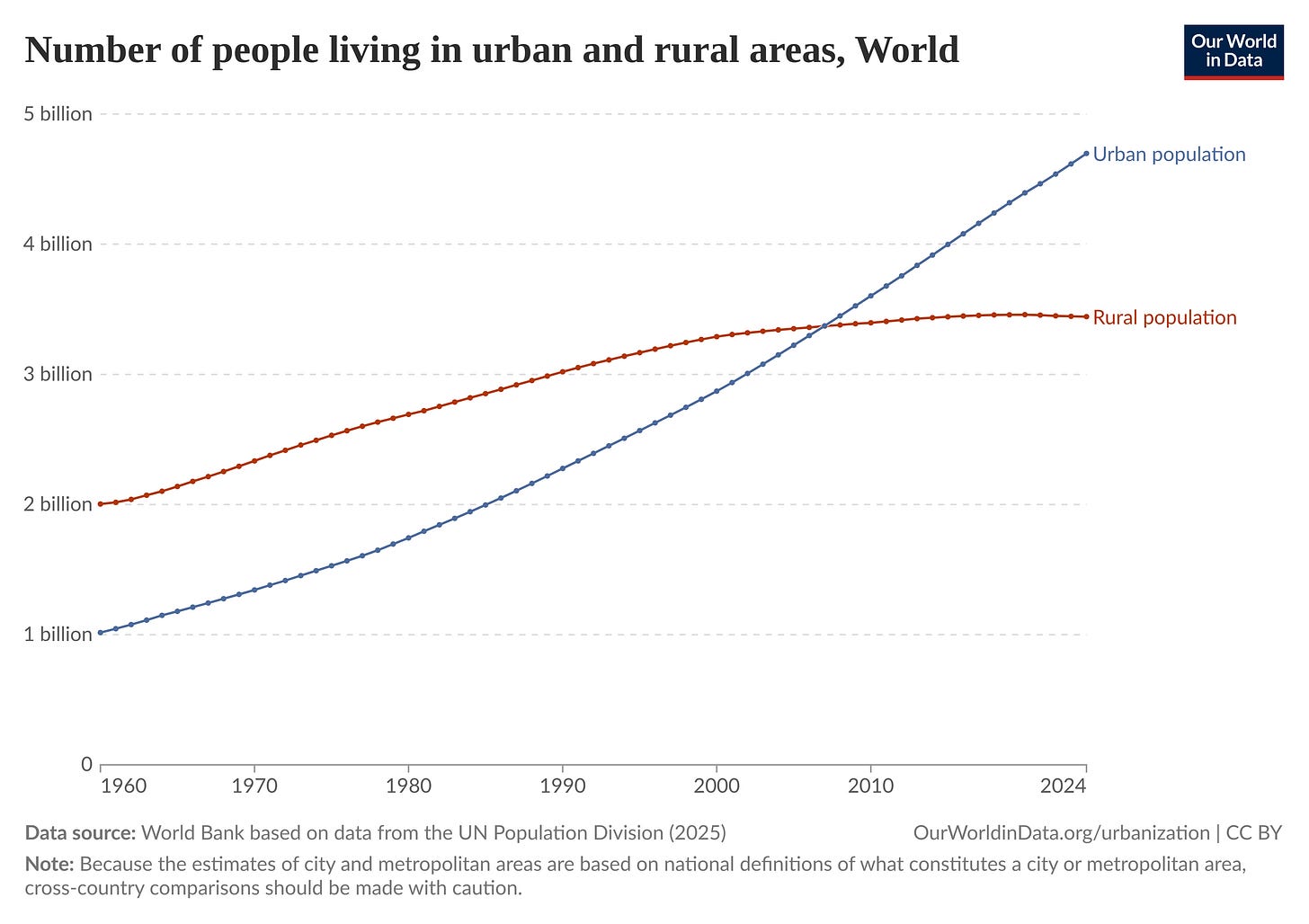

And that new fuel was created and traded in the genuine value factories of our time: great cities. A new wave of urbanization swept the world. Cities grew ever larger; smaller towns emptied out. The educated classes congregated around immense capitals. The assets of societies — investments in both human and physical capital — accumulated around a handful of megacities, often just one or two per country.

When construction slowed and the economy turned digital, the world stopped growing at the pace that those who had designed the system had anticipated. At the same time, the 2008 crisis brought housebuilding to a sudden halt, from which it has barely recovered.

Meanwhile, as productive investment opportunities dried up, the middle classes of developed countries were accumulating ever-larger savings. Pension funds, investment funds, and sovereign wealth funds proliferated, all seeking returns somewhere. Many families also began buying property as an investment.

And central banks, responding to the slowdown in growth, injected hundreds of billions in liquidity into the global economy — causing all that accumulated wealth to grow still further.

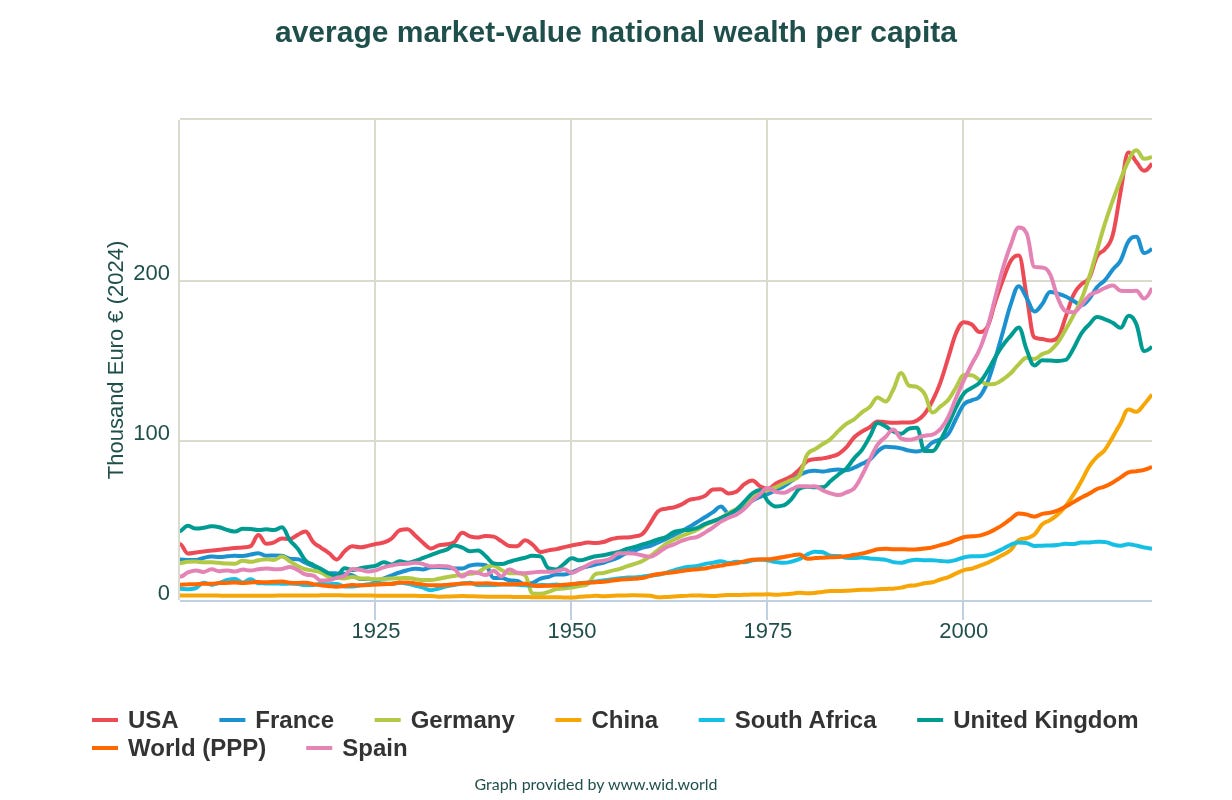

As a result, wealth exploded. It became a mountain with nowhere to invest. And it began to accumulate in housing. The table turned: from being a form of “subordinated capital,” housing became the primary asset class of nations. Today, 60 % of all the world’s wealth is held in real estate, and 50% of all global wealth consists of residential property.

Worse still: all growth since the year 2000 is “paper wealth” — fictitious wealth consisting entirely of the appreciation of the same buildings constructed in the twentieth century. Since 2000, rather than growing by generating value, we have merely had the sensation of “growth” because real estate assets keep rising in price.

Why Is This a Problem?

Because housing produces no value. Unlike factories and construction companies, which drove economic activity — jobs, state revenues, opportunities — and unlike the purchase of new housing, which stimulated construction, the rental or resale of existing homes is the closest thing our world has to the feudal system of the fifteenth century. It produces nothing; it simply functions as a vacuum that extracts resources from the broader economy, channelling them directly into producing more wealth and more accumulation.

This is not, as is commonly claimed, a problem of habitability, or even of rent prices. It is a crisis of wealth distribution and of the “capital” of nations. It is a problem of citizenship.

And in reality it affects tenants and new buyers in almost equal measure. The underlying problem is this: for the generation that purchased the twentieth century’s shares to receive a return commensurate with their expectations — expectations calibrated to a world in which growth had not stopped — another generation must foot the bill. And in “country-companies” that produce far less than before, what happens is that younger generations must devote an ever-greater portion of their time and their lives to buying the “shares” of their country from the generations that came before them.

And if wealth no longer generates more economic activity, it can only end up devouring what remains. If the twentieth-century model was circular — investment produced employment and resources that justified a return — the twenty-first-century model is a Ponzi scheme. Each generation is compelled to make a greater sacrifice to compensate the previous one, until the whole thing blows apart. Meanwhile, the underlying moral logic is terrifying: it endorses a world in which it is far more profitable to be a landlord than an entrepreneur.

This is the tension. We have run out of a model that works for everyone. One generation received a universal inheritance in the form of shares in their country; now every subsequent generation is expected to devote an enormous share of its resources to compensating the previous ones for those shares. This is why housing consumes an ever-larger portion of household budgets. Fifty years ago, housing might represent between 5 and 10 percent of a family’s expenditure; today it reaches 50 percent — and beyond — in many places.

We are playing that game in which a group of people standing in a circle pass around a device with an internal clock — like a time bomb. The moment will come when it is no longer sustainable, and it will explode.

Why Was the Lack of Rental Housing Once Seen as the Problem, When Now It Seems the Rental Market Itself Is?

The traditional housing problem, up until the end of the twentieth century, was one of supply: because so little was paid for housing, there were no development companies, no thriving industry. It was largely people who built their own homes by hand. This is why states needed to build public housing in the twentieth century — no one else wanted to. When tensions began to emerge at the end of the twentieth century and the start of the twenty-first, everyone reached for the old narrative of insufficient supply without thinking much further. But it was not the whole truth.

(Incidentally, constructing a building is very cheap relative to its useful lifespan, which can be effectively infinite. The problem is that we lack financing instruments matched to those timescales, and a tension arises between funding and construction.)

Can Building More Fix the Problem?

Building more is the first step — the equivalent of issuing new shares for the current generation, what in corporate finance is known as a capital increase. The problem is that the original shareholders would resist. And they already do, everywhere in the world: this is what the NIMBY phenomenon is. When a company issues new shares, it dilutes the value of existing ones.

In my view, building more must be part of the solution. The reality is that since 2008 most countries have built practically nothing, while populations continue to grow and household sizes shrink. There is a genuine tension between supply and demand. But to carry out this new “share issuance,” it is not enough to build on the urban periphery — planning codes must be reformed to increase density, and new generations must be guaranteed access at cost price. The land of the city must be redistributed, not merely extended.

Nor does it work to sell at prevailing market prices, because that simply transfers wealth to land developers rather than to the twentieth-century families the system is meant to serve. For any sustainable system, each generation should be able to access a share of their country’s stock at the same price — measured in terms of the life effort required, if you will. This is the key to making the model fair and sustainable: that the effort required of each generation to access a stake in their country’s capital remains constant.

Can the Market Be “Liberalized”?

The housing market cannot be “liberalized” — in the sense of allowing anyone to build whatever they like on land they own — any more than the issuance of a company’s shares can be liberalized. It would be absurd. The number of licenses in any given urban area depends on the available public services: the capacity of sanitation systems, street lighting, water supply, road networks, and public transport.

Urban planning is essentially the most important law in any country — just as controlling the share count is the first job of a chief financial officer. Before building in any area, a series of interventions must take place, necessarily coordinated by a higher authority: sewage, road building, lighting, utility networks, and so on.

If every developer could do whatever they liked on their own plot, cities would become uninhabitable — people throwing waste into the street for lack of sanitation, cars piling up everywhere for lack of any other means of getting around. It is nonsensical to talk about liberalizing land, unless one wants shanty towns to grow like those in parts of Africa. (If anyone wants to convince me otherwise, I am all ears.)

Can Public Housing Solve It?

That depends on which problem you are trying to solve. If the goal is a welfare solution for a minimum number of people in the greatest difficulty, perhaps 2, 3, or 5% of stock could be provided over a couple of decades. But to me that would be a way of entrenching inequality: leaving the country’s shares in the hands of a few, offering a small subsidy to a few others, while everyone in the middle continues to face the same problem.

If the goal is cities where 50, 60, or 70 % of housing is public and people no longer store their savings in property — that strikes me as science fiction. The only way to achieve it would be to expropriate the entire city and rebuild it from scratch.

In my view, the only problem this idea of “building more public housing” actually solves is a political one: it gives certain parties something to say, and allows them to project the illusion of having a solution, while delivering no real results — because building takes ten or fifteen years, and by then, no one will remember the promise. When anyone advocates for public housing, the right question to ask is: how much, and when? How many homes can the state actually build before the end of this parliamentary term? The answer, I fear, is depressingly close to zero.

Why Did Prices Rise During the Bubble Even Though Far More Was Built?

Because when a company carries out a capital increase to fund investments that are expected to make the company more valuable, the share price rises.

The bubble was the moment when the global message went out that housing would be “the great asset” of the future. It was then that governments — having watched prices appreciate through the final years of the twentieth century, when economic growth figures were still very high — could sell their citizens the idea that this was going to be a bonanza where money would fall from the sky. If housing kept appreciating at 10 percent a year, buying more shares was a fantastic idea.

For states to build extensively without prices rising, they must send the market a clear signal that they will not allow appreciation to outpace the economy.

I repeat: states, which issue the shares, control the price.

How Have Experiments in Rent Regulation and Price Controls Fared?

It is very difficult to compare, because every territory has its own characteristics. But in general I think price controls are effective at limiting rental prices. The problem, as we have discussed, is that rent is not exactly the issue — it is one of its symptoms. So controls are a small patch that does not fully resolve the problem, and can actually consolidate the idea that it is normal to have a society in which half the population are shareholders in their country and the other half are merely tenants.

Is the Intersection of Supply and Demand Really Useful or Economically Accurate When Applied to Real Estate That Can Be Withdrawn From the Market at Will?

Real estate cannot be withdrawn from the market. That is a fiction. As we have seen, homes are licenses — and licenses exist whether the property is occupied or not. The building will continue to appreciate in value even if it is never sold.

Housing prices are in reality set by the issuer — the state — which regulates the market through incentives such as tax deductions and purchase subsidies, and through disincentives such as price caps and property taxes. Exactly as companies issue shares or buy them back to support their price.

Should Purchases by Companies and Non-Residents Be Restricted?

They can and should be — and urgently. There is no logic in allowing the shares of one country to be held by the citizens of another. Even Trump recently signed an executive order prohibiting investment funds from buying single-family homes: “America will not be a nation of renters.” Canada has had a ban on foreign purchases in place for two years; the Netherlands has introduced certain restrictions at the municipal level; and other countries — China and Saudi Arabia among them — prohibit foreign property ownership altogether. This is Democracy 101.

Continue reading »

In order to stay within Substack’s recommended length limits, I have divided this masterclass into two parts. Click to continue with the second part:

It’s for today! Solutions to solve the housing problem before it’s too late.

“The long run is a misleading guide to current affairs. In the long run we are all dead. Economists set themselves too easy, too useless a task if in tempestuous seasons they can only tell us that when the storm is past the ocean is flat again.”

If you are interested in housing issues, don’t miss Hijos del optimismo (Children of Optimism). This book explains how the housing crisis is the result of the immense transformations we are currently undergoing.

It is my first book, the big brother of this newsletter, and a project I have been working on for many years.

You can already order Hijos del Optimismo on Amazon, La Casa del Libro, El Corte Inglés and the publisher’s website, Debate.

You can also read more about me and the story that inspired me to write it.

Photo by Adrian Trinkaus on Unsplash