Landlord Economics: When You Are the New Oil

How can it be that even the big tech companies — which got where they are precisely by inventing extraordinary products — now want to be in the business of renting out computing power?

The original (Spanish) version of this article can be found here.

A few days ago, at a presentation of Hijos del Optimismo (Children of Optimism) in Vigo, a woman asked me the best question I’ve been asked so far. She had really enjoyed the book. But what she wanted to know was what she could do to secure her children’s future — or at least give them the best possible opportunities. What should they study? What skills will be useful to them? What things can they simply not afford to be ignorant of in order to survive in this uncertain world?

The best question, and the hardest one.

I gave her an answer that might sound like a cliché — one day I’ll need to elaborate on it properly and write it down. For me, the only asset that doesn’t depreciate is knowing who you are and how you can be of value to others. So the most important thing is for children to learn what they want and to develop the curiosity to understand what they love. To practice the art of seduction — because in the future, the ability to desire and to generate desire in others will be what moves the world.

But in truth, I should have told her: “My friend, go to the bank, remortgage your apartment at its current value, and use the difference to put down a deposit on another one and rent it out. It doesn’t matter what your children study — what will secure their future is owning lots of little pieces of land very close to a hospital.”

Or, at least, that seems to be where the economy is heading lately.

Because in recent years we have been watching what was supposed to be a “knowledge economy” transform at breakneck speed into a “landlord economy.” And not only because a real estate bubble has been simmering across the entire Western world for 25 years — no. To everyone’s astonishment, the landlord economy is now reaching all the way into the AI technology companies.

This week gave us the best example yet.

The Market Madness

The American stock market has been setting records for a month. Ever since Trump gestured toward ending the war with Iran and reopening the Strait of Hormuz, markets have been gripped by a bull market fever. Right in the middle of that bonanza, on Wednesday, four of the world’s seven largest technology companies — the so-called “Magnificent Seven” — reported their quarterly results.

It was a major economic event, and as had happened on previous occasions, Alphabet (Google), Meta (Facebook), Amazon, and Microsoft once again surprised the market with extraordinary profits — beating even the already-elevated expectations of investors who had come in running hot.

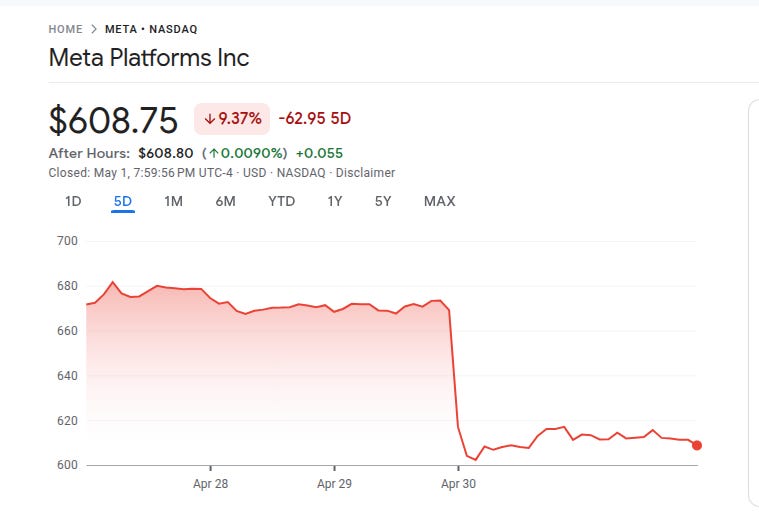

And what happened? The following day, three of the four saw their share prices crash — and the shares of another giant, NVIDIA, fell too

.In a single trading session, Meta — owner of Facebook and Instagram — announced profits 61% higher than the previous quarter and lost nearly 10% of its market value. Microsoft, with 18% profit growth, shed 4%. And NVIDIA, which wasn’t even reporting results, dropped another 4%

How Can This Be?

The explanation for this apparent contradiction is this: the AI bubble has already burst. The speculative moment during which the whole edifice could be sustained on vaporous promises — that it would produce a third industrial revolution and replace 300 million jobs worldwide — has run its course. We have moved from a moment of infinite expectations to one where the actual business and the real economic growth this technology can produce must be measured in facts and, above all, in transactions. That is why Claude Code — the first product after chatbots to achieve genuine market acceptance — marks the end of the AI bubble, for better or for worse.

For those interested in the detail, this week Ed Zitron ran the numbers: “The AI economy doesn’t make sense” and The Verge published a piece I’d also strongly recommend.

Now the question everyone is asking is: which companies will succeed in selling LLM services? Which ones will fall by the wayside? What exactly is the product they’re going to sell? At what price? In other words:

What is the AI business model?

The answer might surprise you.

As we explored a few days ago, everything we call “AI” consists of a new machine learning technique — which is to say, a new type of software. Like all software, it has one major disadvantage when it comes to becoming a big business: it is universal. It cannot be restricted through patents or intellectual property law. As a result, many companies are already building their own AI models. Some are well known — ChatGPT, Claude, Gemini, DeepSeek — but there are many more. Hundreds.

Some are surely better than others, but the expected pattern is that as they evolve, they will also converge in capability. That is how technology works: at first, the inventor has an advantage, but over time others learn to develop it and everyone ends up with roughly the same thing. That is why the first phones were all Nokia — but eventually hundreds of manufacturers emerged, and today all smartphones are remarkably similar. Moreover, the more people in the world who can understand and create a technology, the faster that convergence happens. Today, innovations travel from country to country at the speed of light. There is no reason to believe that any AI model will remain substantially better than all the others for very long.

So the companies in this sector have a problem. In business jargon, there are no “moats” — like the ones around medieval castles — in this industry to keep competitors away from your customers. If you can do it, someone else can copy it and sell it cheaper.

That doesn’t mean these businesses aren’t viable: niche LLMs could exist, tailored to specific and specialized uses, just as different enterprise or HR management software packages exist. But if that were the case, it would be without concentration — a few players couldn’t capture all the returns. You can’t build the next Google by making LLMs adapted to tiny use cases. The end market would look a lot more like HR software or data management software: many relatively small companies each holding small slices of total demand.

And they certainly couldn’t justify the immense valuations — equivalent to many trillions of dollars — they have achieved. To put the scale in perspective: at the end of 2025, the “Magnificent Seven” — Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla — were worth more on the stock market than the entire Chinese economy. Nvidia alone, a company that barely anyone outside the gaming world had heard of five years ago, is today worth more than Germany’s GDP. And that’s before counting private investment: OpenAI, which was valued at $29 billion in 2022, was valued at $850 billion at the end of 2025 — nearly thirty times more in three years — and Anthropic is on a similar trajectory. None of this holds together if LLMs are a normal software business.

The major international capital players are well aware of this minor problem. It’s Investing 101 — the question any venture capitalist asks when you come looking for startup funding. So nobody is investing in these macro companies because they have a particularly good LLM.

So why hasn’t the bubble burst, now that it’s become clear that AI wasn’t going to produce an industrial revolution?

Sam Altman, the current head of OpenAI — who came from working at Silicon Valley’s most famous incubator — knew perfectly well that without a moat he had no business. So when he launched ChatGPT, he invented one. That story Altman told has ended up producing not just the AI bubble, but a transformation in the very nature of the global economy.

The idea was this: LLMs, he claimed, improve linearly the more computing power they have. The difference between a very good LLM and a mediocre one is the processing capacity available for training and generating responses. In other words, the power and effectiveness of AI models depends on hardware, not software.

If reading that sentence doesn’t give you a tingle in your stomach, you’re probably not an investor. Because what they call the “scaling laws” of AI is the holy grail of twenty-first century capitalism.

Until now, every digital technology had the same problem: there are no moats in ideas. But if the scaling laws hold, LLMs would be the first digital technology whose capability depends on a physical and limited resource: the latest-generation chips installed in data centers. Competition would no longer be for code that anyone can rewrite, but for silicon, gallium arsenide wafers, cooling systems, and the gigawatts of power needed to run them. AI would be a supremely powerful technology — capable of replacing humans — but bound, just like them, to physical and material needs that can be controlled and traded. Digital technology, at last, made scarce.

And as if that weren’t enough, the latest-generation chips were also… scarce. Only one company — NVIDIA — manufactured the best ones. Unlike others, NVIDIA has an enormous moat: it has built a programming environment for managing those chips into which tens of thousands of developers have invested enormous amounts of time and money. It has a captive market.

And so the financial world — and above all, the US establishment with Donald Trump at its head — began to see AI as the next frontier, the Wild West, a new virgin territory to be conquered and settled.

The Digital Gold Rush

Since then, the “hyperscalers” — the name given to the companies investing in data centers, encompassing the Magnificent Seven and other players like Oracle and AMD — have launched into an endless race to claim all the available “territory.” Like money cowboys, they are pouring billions of dollars into staking their claims before anyone else plants their flag.

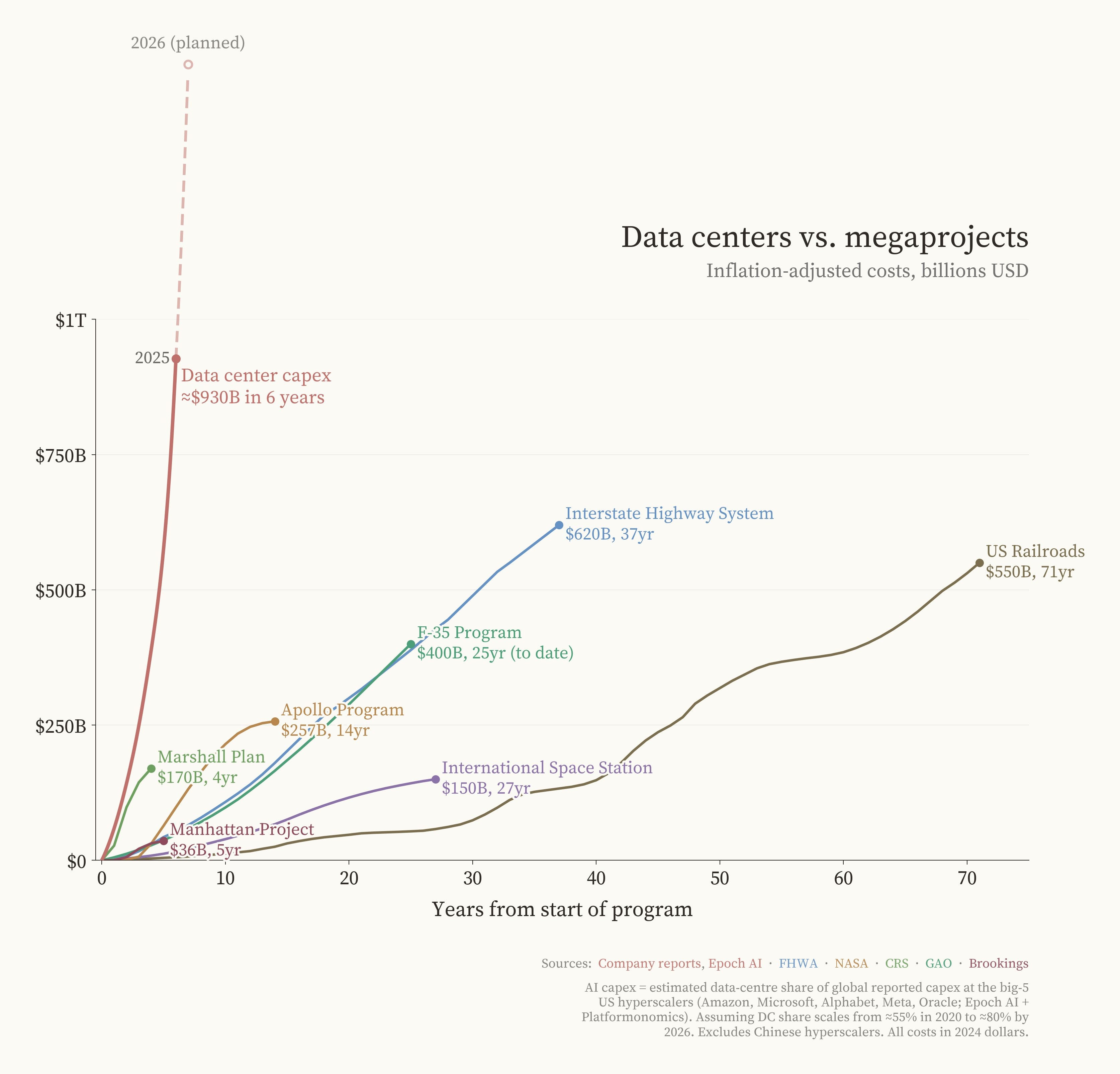

This year alone, they estimate they will spend $700 billion. That figure could reach $3 trillion within five years. Never before in history — not with the railways, not with electricity, not during the Apollo program — has an investment of this magnitude taken place. The digital gold rush is so extreme that investment in these technologies alone accounts for 40% of last quarter’s US GDP growth

The Landlords of Artificial Intelligence

If any of this sounds familiar, it’s because you were paying attention. What is happening with data centers is the same thing that has been happening in the real estate market for years. In that sector, prices have never stopped rising through pure asset appreciation — because more and more capital is seeking position in a market understood to be permanently scarce, one that won’t be digitalized away anytime soon.

The hyperscalers are not investing $600 billion a year because they have a product to sell — in fact, most of them are still losing money on AI. They are buying digital land before it runs out. What they are calculating is the rent they will be able to charge their customers over the coming decades. Economists call this a “scarcity rent” — a return earned not by producing anything new, but by controlling a resource that others need and cannot obtain elsewhere.

So the Magnificent Seven of the American stock market, and the entire AI bubble, are the result of transplanting into the digital economy the same logic that gave us the housing bubble. They don’t want to be the “new intelligence.” They want to be its landlords. The landlords of artificial intelligence

The question, of course, is the same one any real estate investor asks: will there really be enough tenants to pay for all of this? If the scaling laws hold, the data center landlords will be rich. But if they don’t — if models stop improving, if demand fails to materialize, if a technique emerges that requires less hardware, or if chips become cheaper and more manufacturers enter the market — what will remain is a landscape full of empty warehouses stuffed with obsolete chips. Just as Spain was left, after 2008, with those half-built industrial estates and those brand-new apartments on the outskirts of every city that nobody ever moved into.

Landlord Economy: When You Are the New Oil

But the question for everyone else — the cautionary light at the end of all this — is a different one: why is the economy turning into a landlord business? How can it be that even the big tech companies — which got where they are precisely by inventing extraordinary products, the iPhone, the Tesla Model 3, Google Search — now want to leave all that behind and go into the business of renting out computing power?

The answer is a great taboo — one every economist knows but nobody dares say out loud: digital technology does not produce more economy. It produces less. Since the early years of this century, when the spread of the internet coincided with the coming of age of the first university-educated generation, every new digital innovation has swept away a whole range of products and services that were previously provided by the market. Wikipedia liquidated an entire sector of encyclopedias and reference books. Google Maps finished off the street atlas. WhatsApp evaporated billions of euros that we used to spend on SMS messages and international calls. Spotify and YouTube did the same to the music and video rental industries. Craigslist and property portals gutted the classified advertising sections of newspapers, which had been responsible for half their revenue. Each of these innovations produced enormous benefits for users — but in strictly economic terms, measured in jobs, companies, and turnover, they subtracted far more than they added.

And so we have arrived at a point where everyone knows that the more things AI — or any other universally available technology — can do, the fewer jobs and companies will be needed to do them. It is not that machines compete against people: it is that knowledge competes against the economy. Because knowledge is an abundant good that expands without limits, while the economy is a mechanism for managing scarcity.

And this process is only just beginning. So in an uncertain world, where nobody knows what will still be standing in a few years’ time, the bet of those who hold capital today is a land grab — a gold rush, a conquest of the West at any cost. A race to acquire the assets people will need no matter what: urban land, water and gas and electricity distribution networks, ports, and data centers.

Capital, which once sought oil fields confident that someone would eventually buy the barrel, today seeks fields of human beings. You are the new oil.

Drowning in Savings

The tragic thing about all of this is that it is nobody’s fault — or if it is, it is everyone’s. At the end of the twentieth century, wealthy societies made a reasonable decision: to guarantee pensions, health insurance, children’s education, and a stable old age, people needed to save. A lot. And so they did. For decades, millions of people deposited, month after month, a portion of their wages into pension plans, investment funds, life insurance policies, and bank accounts.

The plan was that this money would be lent to companies that would produce things, and from that production would come the returns to pay for retirement — while also generating more industry and more jobs. The problem is that today there is vastly more saved capital than the real economy is capable of absorbing. The mass of money seeking a return far exceeds the productive investments available, especially in a world where, as we have seen, the economy tends to shrink rather than grow.

But that money — without any better explanation, guided by the same mantras that told the twentieth century of the virtue of saving — demands a return that the economy can no longer provide. So it goes looking for it elsewhere, and the only guaranteed return it can find is in rent-seeking.

This is the trap we are in. Savings, which were supposed to be a safety net, have become a tsunami threatening to drown what remains of the economy.

And the reason the bubble will burst — and will keep bursting again and again until we find a remedy — is the same reason it burst in 2000 and in 2008: this is only the third act of the same bubble. A moment will come when the capital poured into AI discovers there is not enough demand on the other side. Just as there weren’t enough customers for the dot-coms, and just as there weren’t enough solvent buyers for apartments in 2008. There are not, and will not be, enough users capable of paying the rent that data centers need to justify the billions invested in them. Not because the technology doesn’t work — that remains to be seen — but because, even if it does work, what it will do is shrink the economy, not grow it. And a shrinking economy cannot sustain indefinitely a capital that only wants to expand.

Reasons for Optimism?

I find myself with a very strong sense of end of cycle. We are at a point in history where, whatever happens — whether AI succeeds or fails, whether the Democrats win the midterms or not — extraordinary changes are coming, because all the formulas that worked until now have run their course.

I think almost everyone has the feeling that their life is going to change in the coming years. And that is not a bad thing — on the contrary, it is an opportunity to make decisions we probably should have made decades ago.

The most important thing, in my view, is to stay informed — because that is how we know we have the capacity to act — and to stay connected with others, so that fear doesn’t get the better of us.

So… until next time!

If this topic interests you, you can’t afford to miss Hijos del Optimismo (Children of Optimism) — a book that explains how the housing crisis and the AI bubble are the consequence of the immense transformations we are living through today.

It’s my first book, the older sibling of this newsletter, and a project I’ve been working on for many years.

Hijos del Optimismo (Children of Optimism) is available at your favorite bookshop — including Amazon, Casa del Libro, El Corte Inglés, and the publisher’s website, Debate.

You can also read an excerpt here

.